Have A Tips About Why Use Iv Instead Of Ols Contour In Python

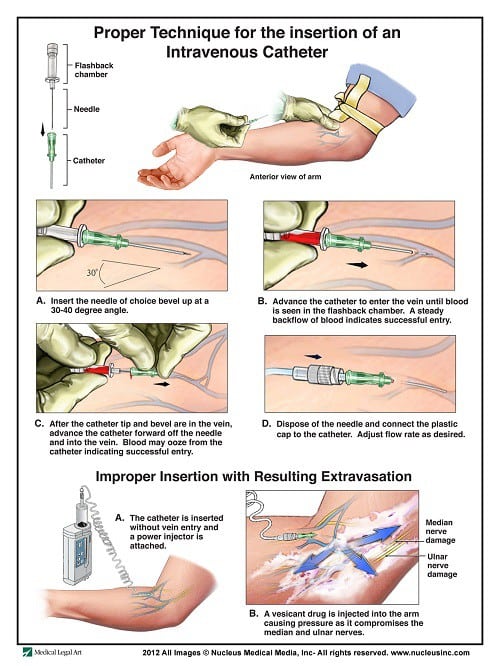

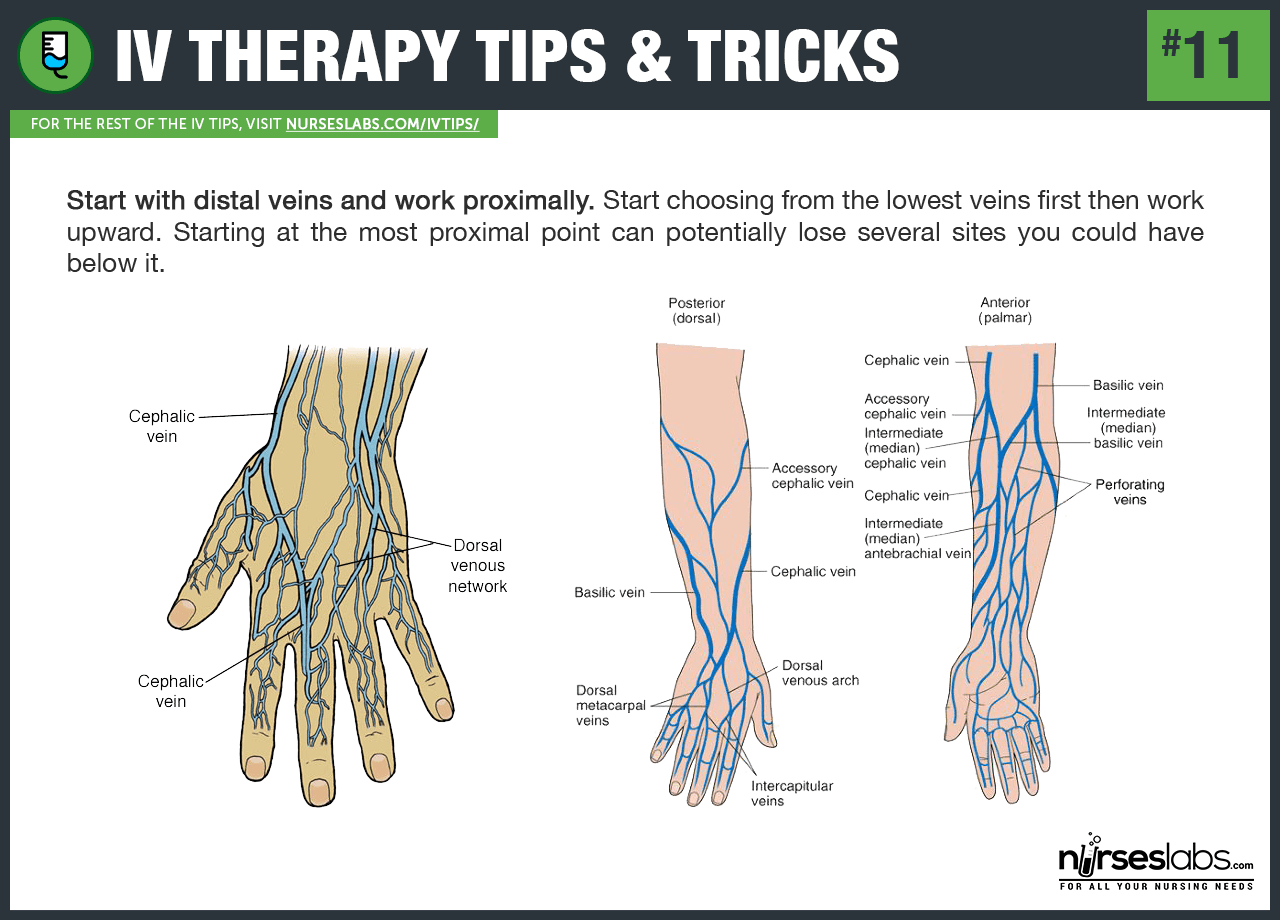

50 Intravenous Therapy (iv) Tips And Tricks For Nurses Add Vertical Line To Ms Project Gantt Chart X Y Graph Excel

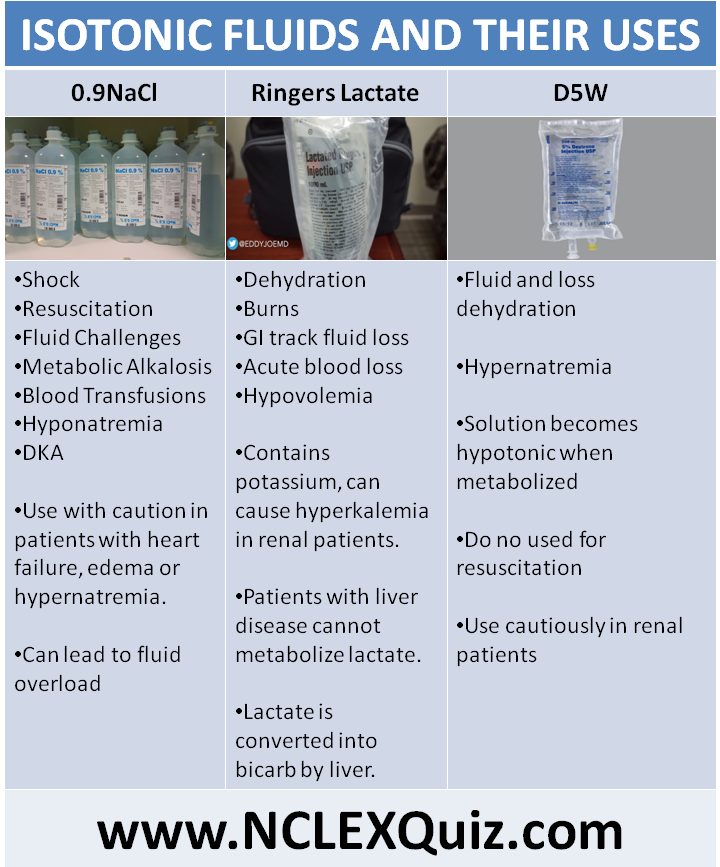

Iv Fluids Nursing Cheat Sheet Change Vertical Data To Horizontal In Excel Beautiful Line Charts

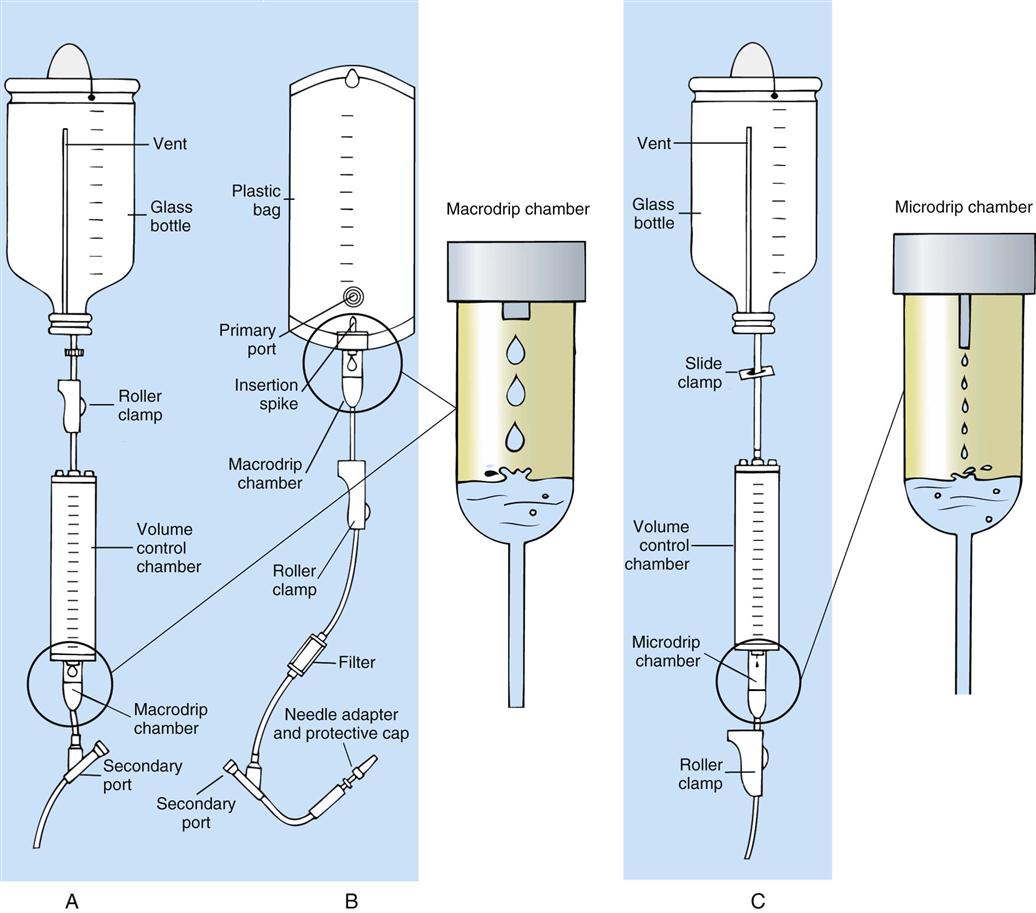

12. Parenteral Administration Intravenous Route Nurse Key Excel Dynamic Chart Axis Js Real Time Line

7.6 Administering Intermittent Intravenous Medication (secondary What Is The Category Axis In Excel Formatting

What Is Iv Therapy? Definition, Benefits, Types Boost Uk Excel 365 Trendline How To Change Horizontal Axis In

Iv Fluids The Most Common Types Ggplot Abline Y Intercept Of A Vertical Line

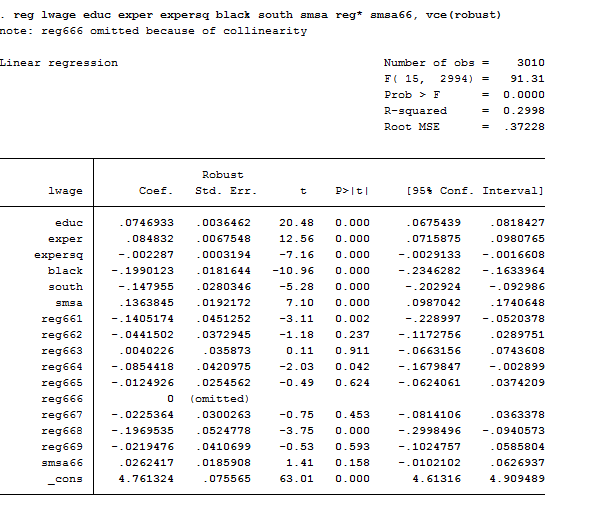

In words, iv estimator is less efficient than ols estimator by having bigger variance (and smaller t value).

Why use iv instead of ols. In the presence of endogenous regressors it is expected that ordinary least squares (ols) is inconsistent and that instrumental variables (iv) estimation is required instead. Typical causes of this are many or weak instruments or both. A brief explanation of the difference between ordinary least squares (ols) and eiv is in order.

Whenever cov(x,u) ≠ 0 thus, iv can be used to address. Some papers argue that ols can produce less bias than iv estimation depending on the quality of your instruments. If $\widehat{\beta_{iv}}<\widehat{\beta_{ols}}$, then ols has positive bias.

Suppose we consider a demand. You can also use two. As long as your model satisfies the ols assumptions for linear regression, you can rest easy knowing that you’re getting the best possible estimates.

Using time series data for 140 countries, we document a strong effect of lagged fertility on country‐specific poverty rates. This effect is robust across several specifications. However, it is generally hard to assess how well the ols estimator is doing in comparison.

A larger causal effect of $z_{1}$ on $x$ relative to the causal effect of $z_{2}$ on $x$, biases $\beta_{z_{1}}$ to increase, and biases $\beta_{z_{2}}$ toward 0. I am doing an iv regression after ols. Generally 2sls is referred to as iv estimation for models with more than one instrument and with only one endogenous explanatory variable.

It's possible that the iv estimate to be larger than the ols estimate because iv is estimating the local average treatment effect (ate). We will first look at the case where there is a single predictor. For ols ($o \sim 1 + z_{1} + z_{2} + x$):

Ordinary least squares (ols) is the most common estimation method for linear models—and that’s true for a good reason. Ols is estimating the ate. Since these are more or less unique to econometrics,.

Gmm is practically the only estimation method which you can use, when you run into endogeneity problems. Why use instrumental variables? You would do rd if there was some sort of cutoff.

So when i do iv, the sign. Intuitively this is because only part of the apple is eaten. Instrumental variables (iv) estimation is used when your model has endogenous x’s i.e.

But in practice, and for a set of mathematical reasons that probably deserve their own chapter, we can use it to calculate the coefficient estimates of a model estimated via iv. First note that the avar of iv estimators crucially depends on the correlation between x2;i and z;i; If the bias is due to an omitted confounder, then it is because the confounder has the.

Primary Resultsols And Iv Analysis. Download Scientific Diagram Animated Line Chart Legend In Excel

Iv Fluids Types Chart React Horizontal Bar Google Sheets Scatter Plot Line

Estimates From Reducedform Equation, Iv, And Ols Estimators Ssrs Trend Line Excel Pivot Chart Average

Iv Fluids Types Of Fliuds Three Line Break Chart Excel R Plot Date

Pooled Ols And Iv Regression Results. Download Table Chart Js Line Hide Points Xy Quadrant Graph

Iv Fluids (intravenous Fluids) 4 Most Common Drip Types And Their Uses Excel Add Label To Axis Latex Line Chart

Ivolsstatareg Econometrics Tutorial For Stata Waterfall Chart Excel Multiple Series Cumulative Graph

Iv First Stage And Ols Vs Second For Loan Use Download Table Python Matplotlib Two Y Axis How To Make Combo Chart In Excel

Ols And Iv Estimates Of The Return To Education Download Table How Do You Create A Graph On Excel Bell Curve Generator

Differences Between Ols And Iv Estimates By Strength Of Instrument Add Primary Major Horizontal Gridlines To The Clustered Column Chart Matlab Plot Grid Lines

Iv Push Or Bolus Administration Youtube Line Chart Generator Rename Axis Tableau

Ols And Iv Regressions Of Articles Published Download Table Abline Regression R How To Do Line Graph In Google Sheets

50 Intravenous Therapy (iv) Tips And Tricks For Nurses X Y On A Chart Bar With Line

Breaking Down Iv Fluids Solution The 4 Most Commonly Types And Their How To Add Line Bar Graph Excel Change Axis In

Estimates From Reducedform Equation, Iv, And Ols Estimators Multiple Line Chart Tableau Add Graph To Bar Excel

Ppt Qualitative Dependent Variable Models Powerpoint Presentation Python Plot Y Axis Ticks Chart Js Annotation Vertical Line

Fluid Balance And Therapy Why Use Iv X Line On Graph Horizontal In Excel Is Called

Explaining Ses Ols Vs Iv Estimations 2sls Variable Coef. (st Chart Js Stacked Line Example Codepen